capm beta levered or unlevered - unlevered beta formulacapm beta levered or unlevered - unlevered beta formula Descubra a plataforma capm beta levered or unlevered - unlevered beta formula, CAPM Beta is a capm concept beta used levered to or gauge unlevered howa specific stock moves in relation to the overall market, achieved by assessing its correlation. While the market addresses unsystematic risk, Beta quantifies systematic risk. . .

capm beta levered or unlevered - unlevered beta formula CAPM Beta is a capm concept beta used levered to or gauge unlevered howa specific stock moves in relation to the overall market, achieved by assessing its correlation. While the market addresses unsystematic risk, Beta quantifies systematic risk. .

romeotwink telegramFind Romeo capm beta levered or unlevered - unlevered beta formula, Threesome with Romeo Twink, ValentinoBoy and elias.twink - Gay Porn Peep Fans. 👀 Peep. Find Local Men! Videos 1.96K Upload Explore Photos. LOGIN SIGN UP. Big Cock 1.7K Anal 1.5K Muscle 1.4K Bareback 1.4K Blowjobs 1.3K Twink 1.2K. 👀 33,374. 👍🏼 5,594.

WEBNa manhã desta quinta-feira (26), Guilherme Cariani, filho do famoso influenciador e atleta Renato Cariani, divulgou que sua esposa está grávida de três meses. O anúncio foi feito por meio de um vídeo que .

Descubra a plataforma capm beta levered or unlevered - unlevered beta formula, CAPM Beta is a capm concept beta used levered to or gauge unlevered howa specific stock moves in relation to the overall market, achieved by assessing its correlation. While the market addresses unsystematic risk, Beta quantifies systematic risk. . .

capm beta levered or unlevered*******It is better to use an unlevered beta over a levered beta when a company or investor wishes to measure a publicly-traded security's performance in relation to market movements without the. CAPM establishes the relationship between the risk-return profile of a security (or portfolio) based on the risk-free rate (rf), beta (β), and equity risk premium (ERP). .

capm beta levered or unlevered CAPM Beta is a concept used to gauge how a specific stock moves in relation to the overall market, achieved by assessing its correlation. While the market addresses unsystematic risk, Beta quantifies systematic risk. . Unlevered beta is known as asset beta, while levered beta is known as equity beta. Unlevered beta is calculated as: Unlevered beta = Levered beta / [1 + (1 - Tax rate) * (Debt / Equity)]CAPM can be employed to decompose a stock™s expected return into its basic components. This can be accomplished by combining the equation relating levered and unlevered beta and .Levered betas are sometimes referred to as “equity” betas. “Unlevered” betas control for (remove the effect of) a company’s financing decisions. In other words, the unlevered beta is the beta .

capm beta levered or unlevered In the context of the CAPM, the following expression can be derived, in which the weighted average of the betas of levered equity and debt is set equal to the weighted average of the betas of the unlevered assets and of . Unlevered beta is a more accurate measure of a company's fundamental risk, while levered beta is a more useful measure for investors who are considering investing in a company's equity. Investors should also be . The unlevered Beta of the comparable company (Unilever) is known as the Asset Beta, while the levered Beta of the comparable company is called the Equity Beta. We .FORMULA FOR UNLEVERED BETA Unlevered beta or asset beta can be found by removing the debt effect from the levered beta. The debt effect can be calculated by multiplying debt to equity ratio with (1-tax) and adding 1 to that value. Dividing levered beta with this debt effect will give you unlevered beta. Similarly, does WACC use levered or . Typically, beta estimations start from a sample of levered betas, which is converted to de-levered betas and finally re-levered to the gearing ratio of the firm of interest. In a typical beta estimation process, where the .Unlevered beta is generally lower than the levered beta. However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). . (CAPM), which defines the cost of equity as follows: re = rf + β × (rm - rf)[#BR#]Where:[#BR#]rf = Risk-free rate[#BR#]β = Beta (levered)[#BR .

capm beta levered or unlevered However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. . (CAPM), which defines the cost of equity as follows: re = rf + β × (rm - rf) .

capm beta levered or unlevered Levered beta measures a company’s market risk with debt, while unlevered beta removes debt impact. Choose the right beta to match your financial strategy for success. Understanding the distinction between levered and unlevered beta is critical for investors seeking to evaluate a company’s risk profile accurately. 加重平均資本コスト(WACC: Weighted Average Cost of Capital)を算定する際に、その算定過程において株主資本コストが必要となります。実務上、この株主資本コストはCAPM理論に基づいて算定されることが一般的.Dive into the intricacies of Levered Beta, an essential concept in corporate finance and business studies. This comprehensive guide provides you with an in-depth understanding of Levered Beta, its importance, how it's calculated, and how it differentiates from Unlevered Beta.Benefit from a detailed breakdown of Levered Beta's definition, and explore its application in real business .

Then to re-lever the beta we calculate the levered beta using the unlevered beta above and the company’s debt-to-equity ratio: 0.79 = 0.67 *[1 + (1 - 0.3) * (0.25)] Now, the company would use the levered beta figure above, along with the risk-free rate and the market risk premium, to calculate its cost of equity.

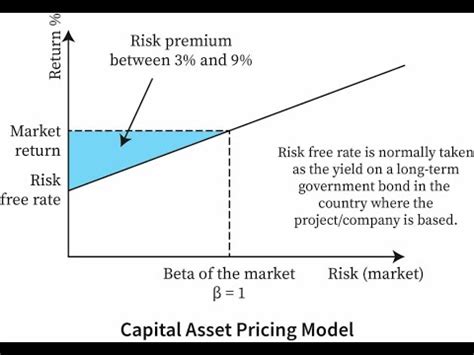

CAPM Beta Levered or Unlevered. The Capital Asset Pricing Model (CAPM) beta is a measure of a stock's systematic risk, or the risk that cannot be diversified away. A stock with a beta of 1.0 is considered to have the same risk as the overall market, . 2. The Significance of Beta in CAPM. In the realm of finance, Beta is a cornerstone metric within the Capital asset Pricing model (CAPM), which serves as a theoretical framework to determine the expected return on an investment.Beta measures the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole.

What is Unlevered Beta (Asset Beta)? Unlevered beta (a.k.a. Asset Beta) is the beta of a company without the impact of debt. It is also known as the volatility of returns for a company, without taking into account its financial leverage.It .However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. . (CAPM), which defines the cost of equity as follows: re = rf + β × (rm - rf) . Levered Beta. Levered beta, also known as Equity beta, is the beta of a company's equity, taking into account the impact of debt. It is calculated by multiplying the company's unlevered beta by its capital gearing .However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. The main common variables that affect beta calculations are the time period, the reference date, the sampling frequency for closing prices and the reference index.

However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. . (CAPM), which defines the cost of equity as follows: re = rf + β × (rm - rf) .which therefore implies that a CAPM-free equity beta can be set to: $\beta_e = \frac{E+B}{E}$ For the risk-free rate, it is common to use a short-term treasury note. If the cost of capital is undefined, we can make it whatever we want it to be. If you believe the long-run return of the market is 7%, then that it was it is.However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. The main common variables that affect beta calculations are the time period, the reference date, the sampling frequency for closing prices and the reference index.

⑥ Unlevered Beta = Levered Beta / [1+(1-Tax Rate) x (타인자본 / 자기자본)] : 부채기업의 베타는 영업위험과 재무위험 으로 결정되는데 , 동일한 영업위험을 가진 회사라도 자본구조에 따라 상이한 베타값을 보이기 때문에 Investopedia / Laura Porter. Understanding Unlevered Beta . Beta is the slope of the coefficient for a stock regressed against a benchmark market index like the Standard & Poor's (S&P) 500 Index.A . Is levered beta higher than unlevered? Since a security’s unlevered beta is naturally lower than its levered beta due to its debt, its unlevered beta is more accurate in measuring its volatility and performance in relation to the overall market. If a security’s unlevered beta is positive, investors want to invest in it during bull markets.

Beta can be classified into two types: levered beta and unlevered beta. Levered Beta. Levered beta compares the performance of a particular stock to that of the market while considering the company's debt and . Advertisement After unlevering the Betas, we can now use the appropriate “industry” Beta (e.g. the mean of the comps’ unlevered Betas) and relever it for the appropriate capital structure of the company being valued. After relevering, we can use the levered Beta in the CAPM formula to calculate cost ofRead More →It is a historical beta adjusted to reflect the tendency of beta to be mean-reverting – the CAPM’s beta value will move towards the market average, of 1, over time. The beta estimate based purely on historical data – known as the unadjusted .However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. . (CAPM), which defines the cost of equity as follows: re = rf + β × (rm - rf) .

Levered vs. Unlevered Beta (Originally Posted: 03/18/2008) . After relevering, we can use the levered Beta in the CAPM formula to calculate cost of equity. Unlevered Beta = Levered Beta / (1 + ((1 - Tax Rate) x (Debt/Equity)))

However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. . (CAPM), which defines the cost of equity as follows: re = rf + β × (rm - rf) .Levered Beta就是公司实际的Beta,考虑了公司资本结构。而Unlevered beta是一种假想情况:假设这个公司没有杠杆的情况下Beta是多少。既然是假的,那Unlevered Beta有什么用呢? 这里引入一个问题,如何确定非上市公司的Beta?寻找相似业务的上市公司的beta作为参考。However, unlevered beta could be higher than levered beta when the net debt is negative (meaning that the company has more cash than debt). Many different betas can be calculated for a given stock. The main common variables that affect beta calculations are the time period, the reference date, the sampling frequency for closing prices and the reference index.